Transparent. Experienced. Reliable.

As trusted marketplace leaders, IPv4.Global is dedicated to reliable, transparent service. IPv4.Global has completed more transfers than anyone else, worldwide: our experience gets results.

IPv4.Global by Hilco Global

IPv4.Global partners with network owners to monetize assets, source scarce resources, conserve capital through IPv4 leasing and facilitate private sales of these vital assets.

We provide sophisticated, world-class IPAM and DDI software. Our consultants help with expansions and transitions of all sorts, including network data normalization and migration, renumbering, and business process automation. And we facilitate the sale and purchase of facilities and lend against the IP assets of mature organizations.

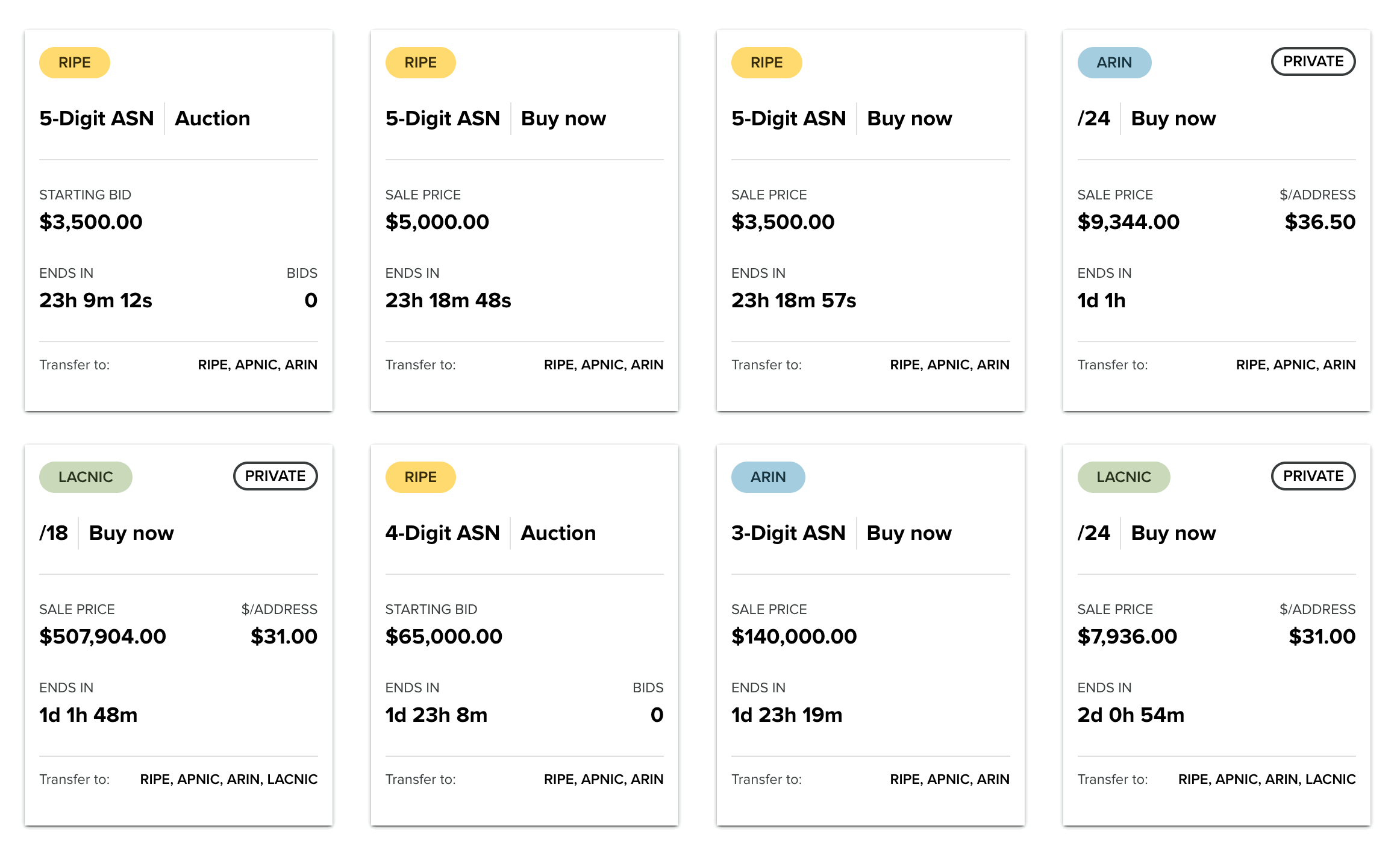

Our Online Marketplace

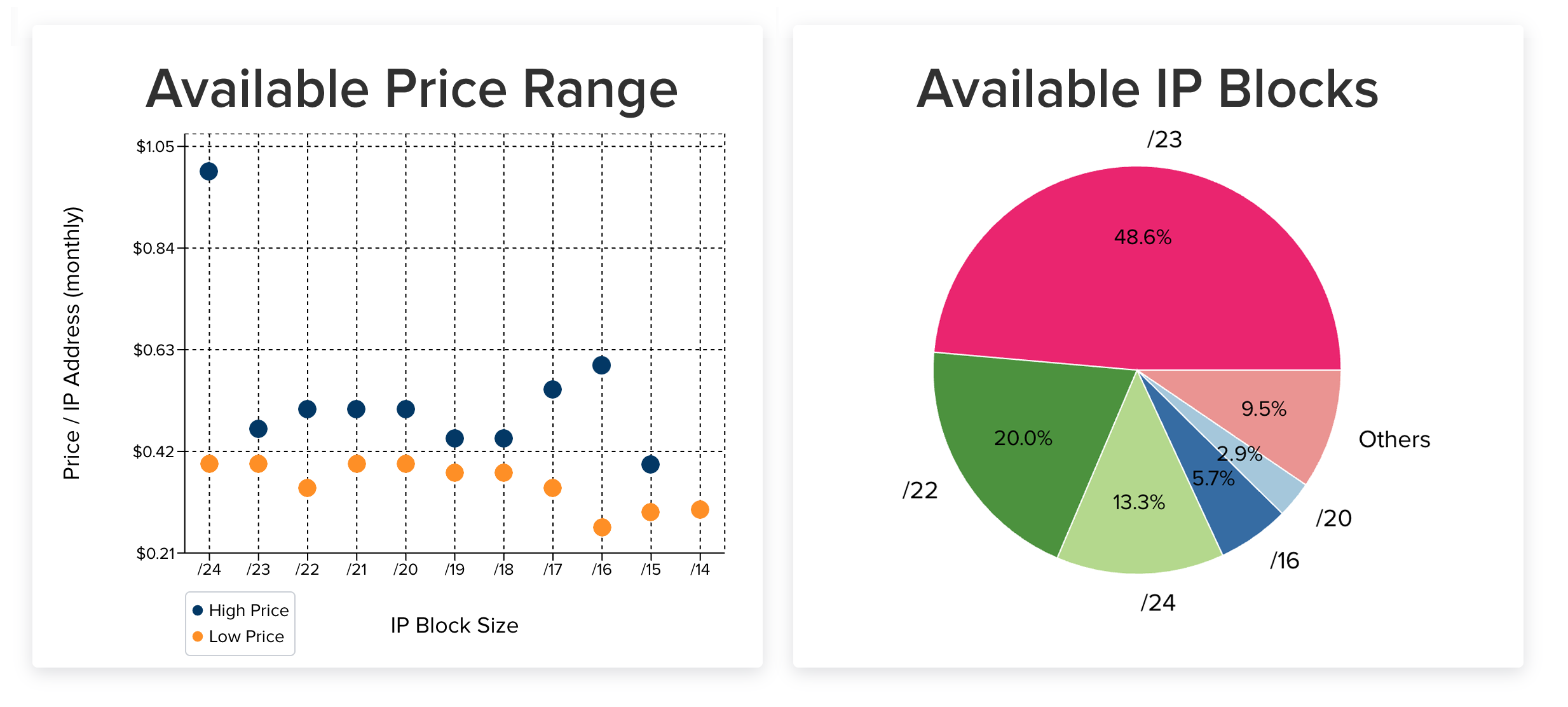

We understand that the concerns of buyers and sellers of large IPv4 address blocks often differ from the needs of those looking to buy and sell smaller blocks. IPv4.Global is an IPv4 broker providing multiple solutions designed to meet the unique needs of IPv4 buyers and sellers of every size.

Our online platform provides buyers and sellers of IPv4 addresses and ASNs with a streamlined and transparent process to transfer the rights to these assets.

Private Brokered Solutions

For those interested in buying or selling IP addresses in large blocks, IPv4.Global provides privately negotiated transaction services. Our team has successfully arranged the sale of millions of IPv4 addresses and are experts on the IP address transfer process. There are no hidden fees.

IPv4.Global Chrome Extension

Track the IPv4 market directly from your browser. Our new Chrome extension provides live updates on marketplace listings, sales, and prices through a convenient ticker display.

IPv4.Global is excited to offer ProVision, sophisticated, world-class IPAM and DDI software. ProVision is an API-first, multi-tenant, multi-cloud solution that automates the complexities of planning, provisioning, and managing modern network infrastructure. It empowers networks of all kinds to scale with precision and speed.

Getting Started

Buying, selling and leasing IPv4 addresses is organized on our marketplace so that information is transparent and easy to find. Qualifications for legitimate buyer and seller participation are simple and direct. Plus, our support staff is always ready to help with the process of buying, selling and then transferring addresses.

For a beginner’s overview of our marketplace and how it works

Leasing IPv4 Addresses

Leasing IPv4 addresses offers a cost-effective and flexible solution for organizations looking to expand their IP resources. Whether you have surplus IPv4 blocks to lease out or need additional IPv4 addresses for short- or long-term use, our IPv4 leasing marketplace connects lessors and lessees for seamless transactions.

0 +

million

addresses brokered

$ 0

billion

generated for our clients

0 +

transactions

since 2014

CUSTOM IPv4 SOLUTIONS

![]() Buyer Registration

Buyer Registration

![]() Registry Record Updates

Registry Record Updates

![]() Inter-RIR Transfers

Inter-RIR Transfers

![]() Long Term Planning

Long Term Planning

![]() Capital Solutions

Capital Solutions

CUSTOMER SATISFACTION

OPERATING IN ALL FIVE INTERNET REGISTRIES