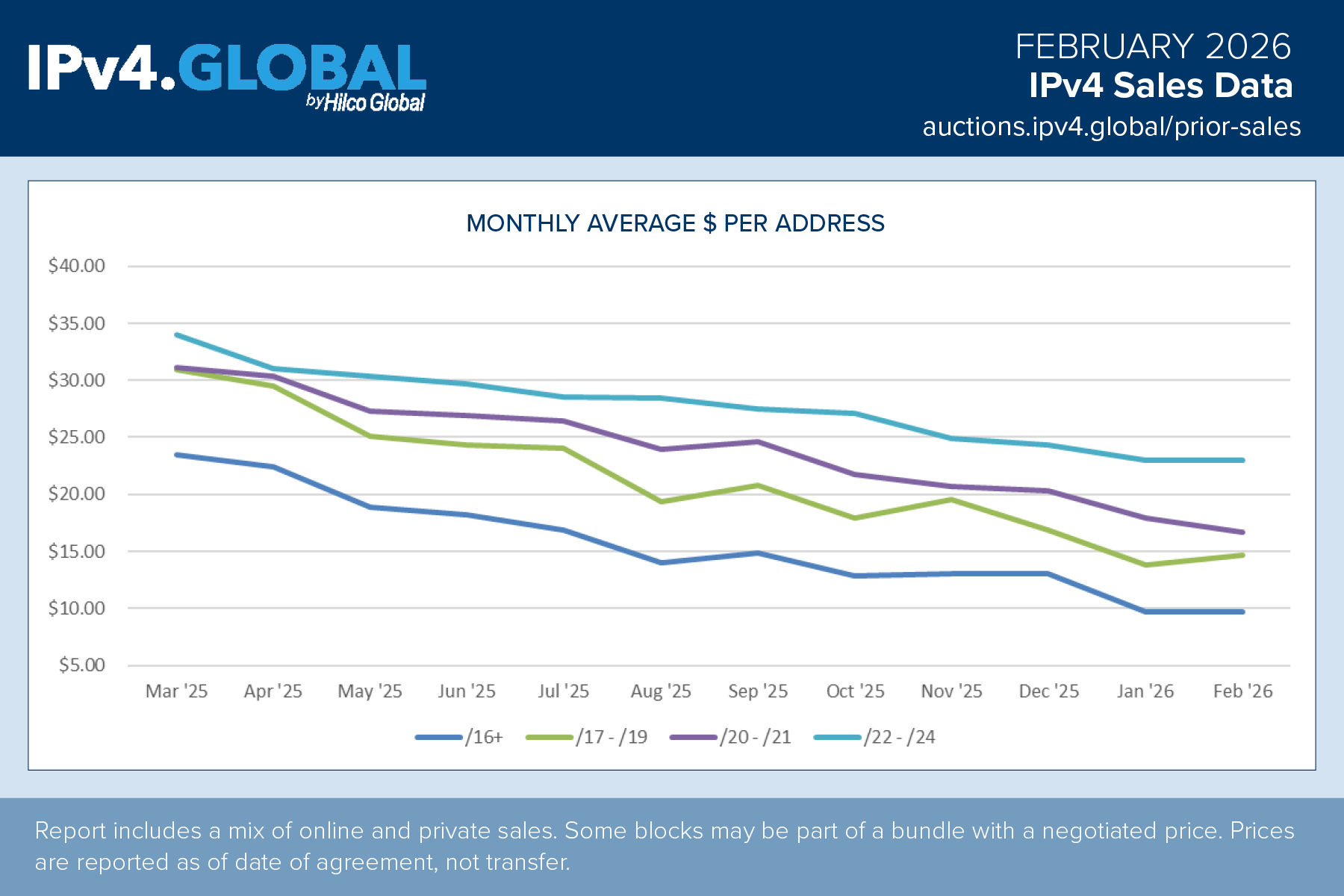

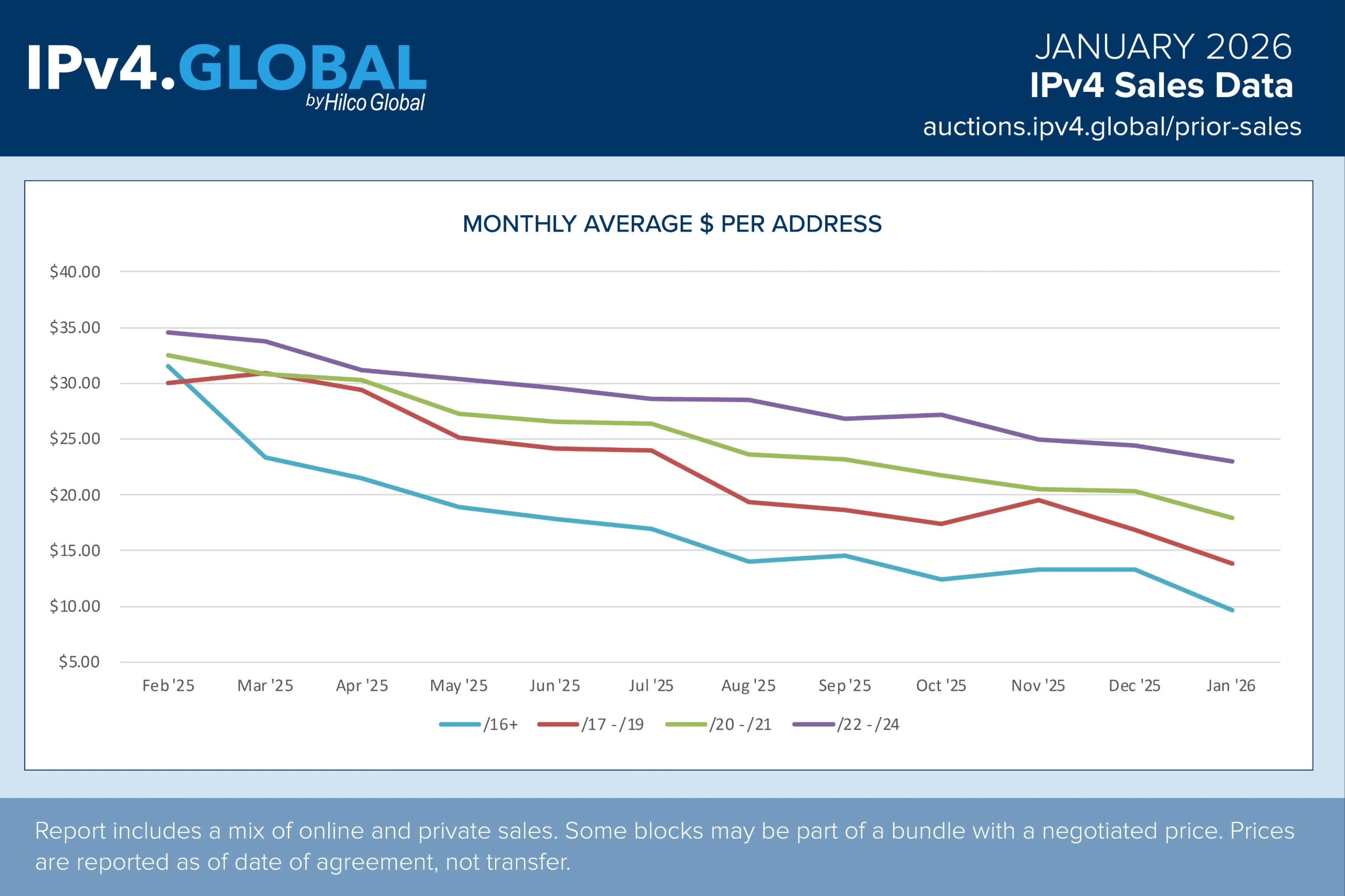

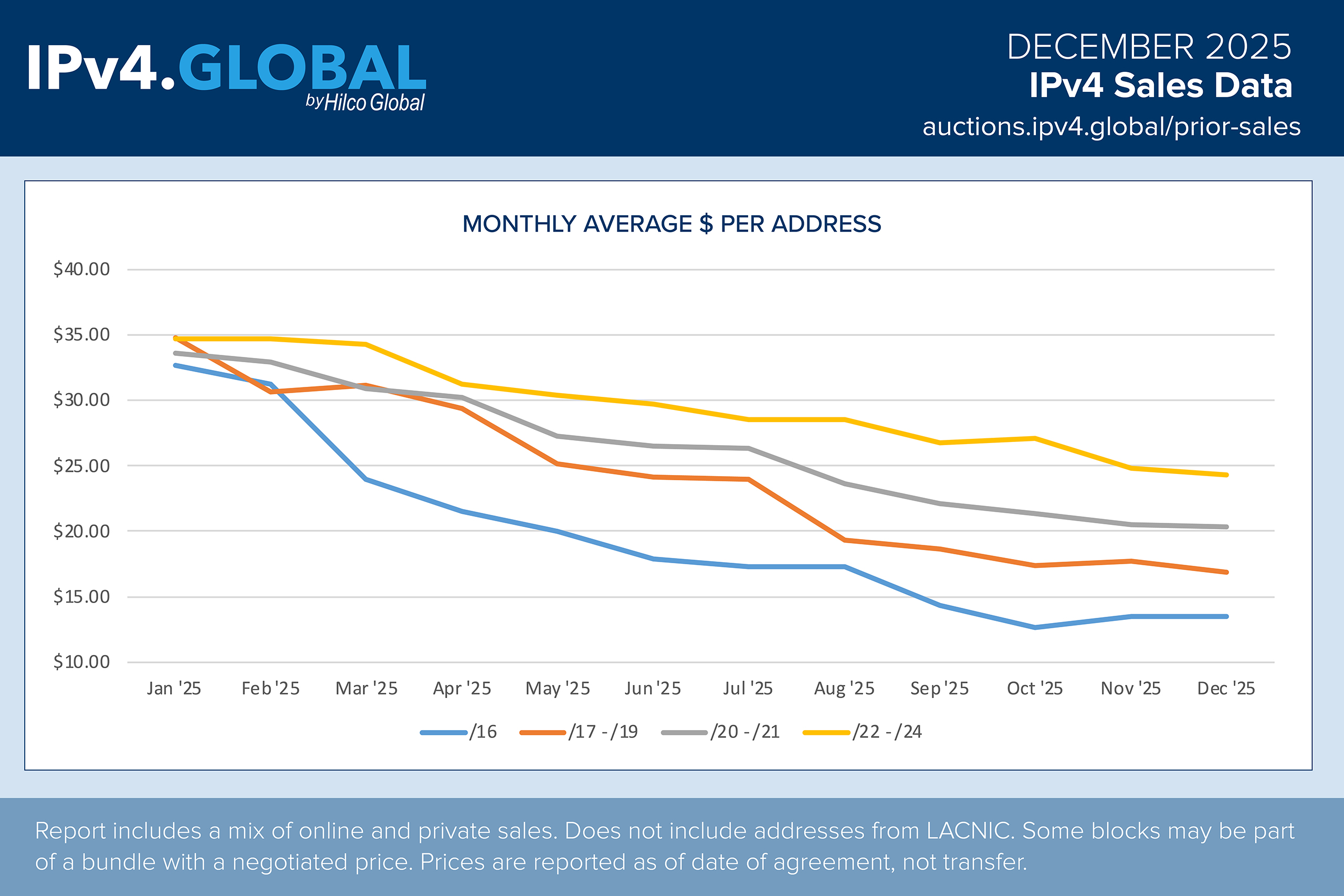

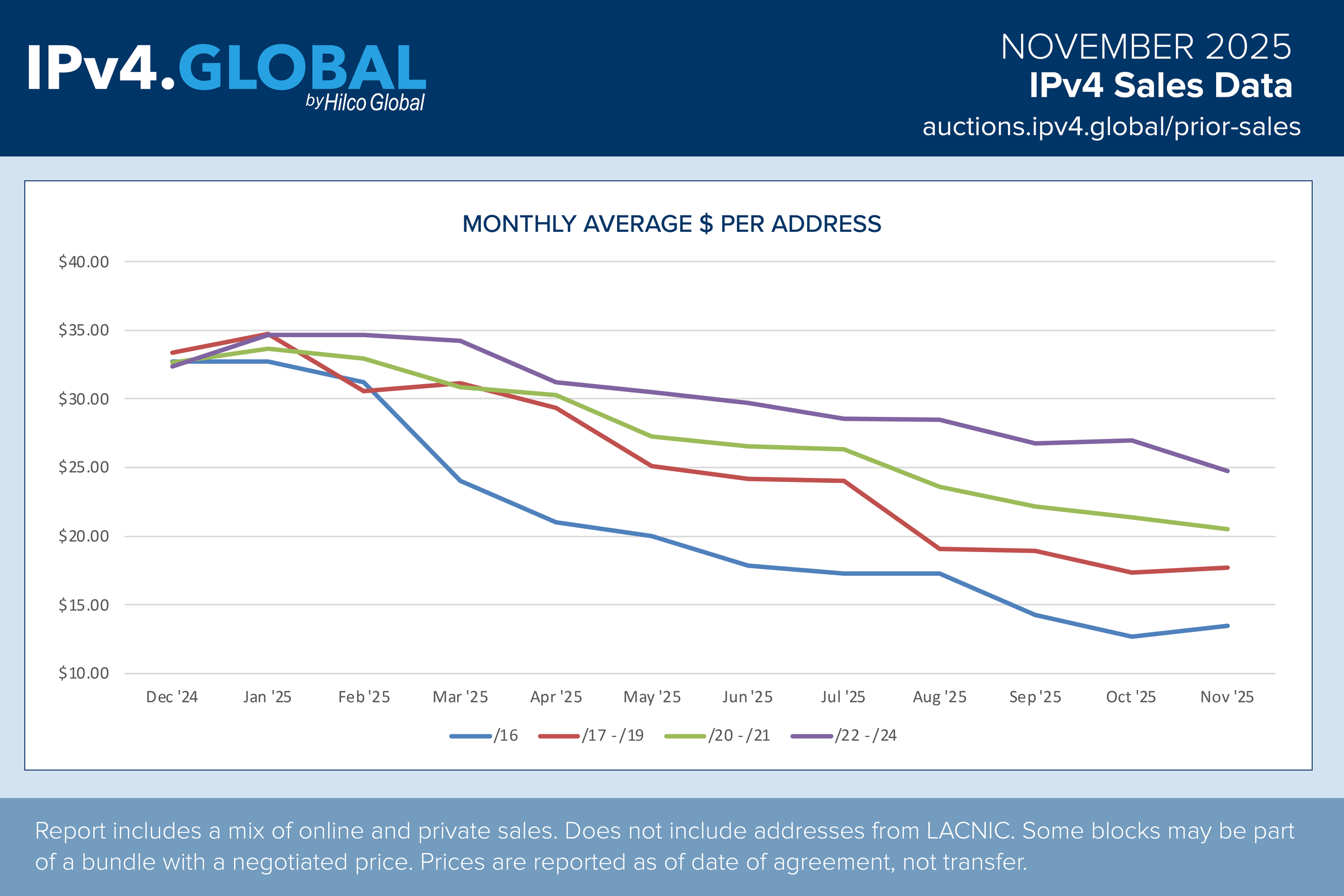

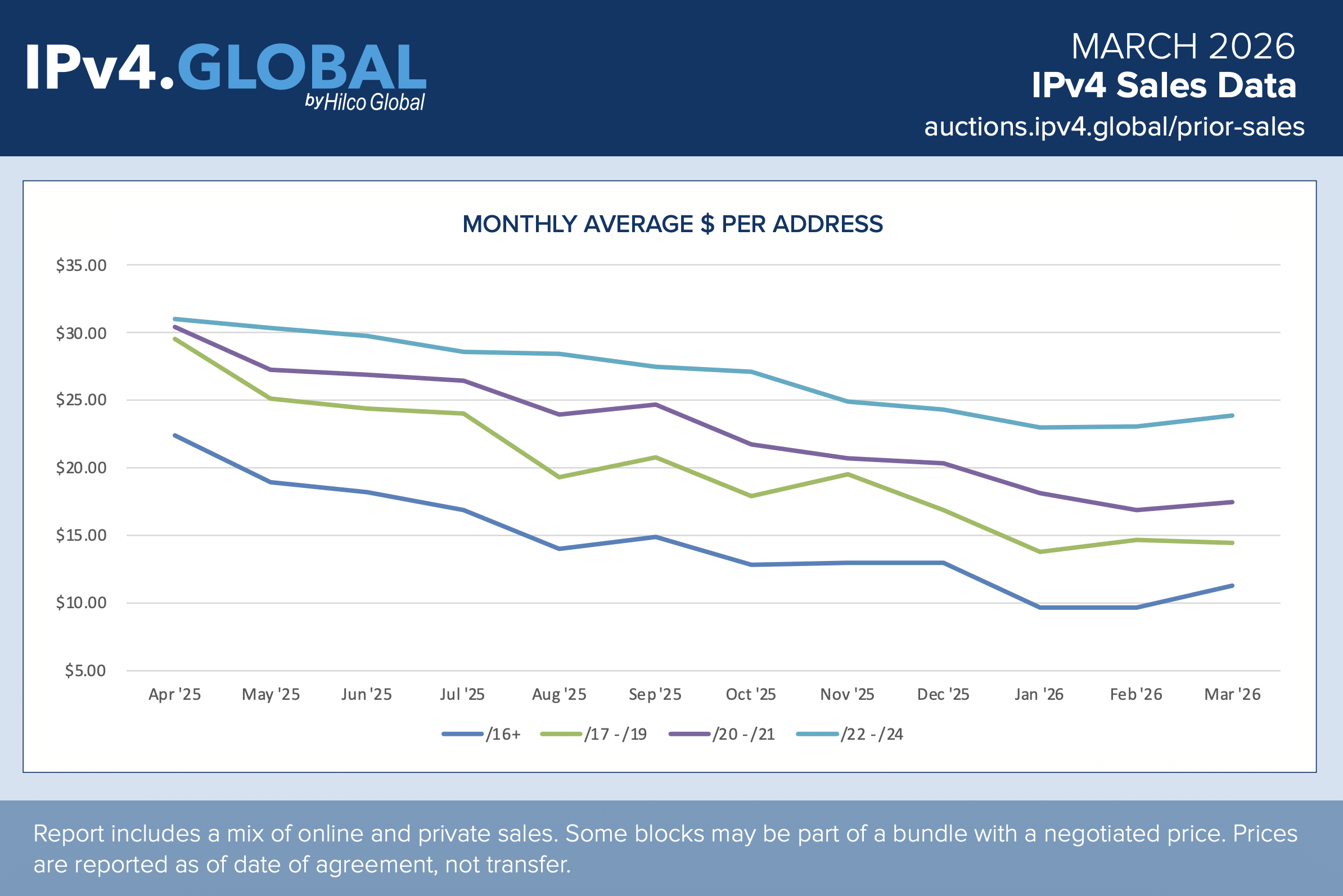

March 2026 IPv4 Marketplace Sales Report

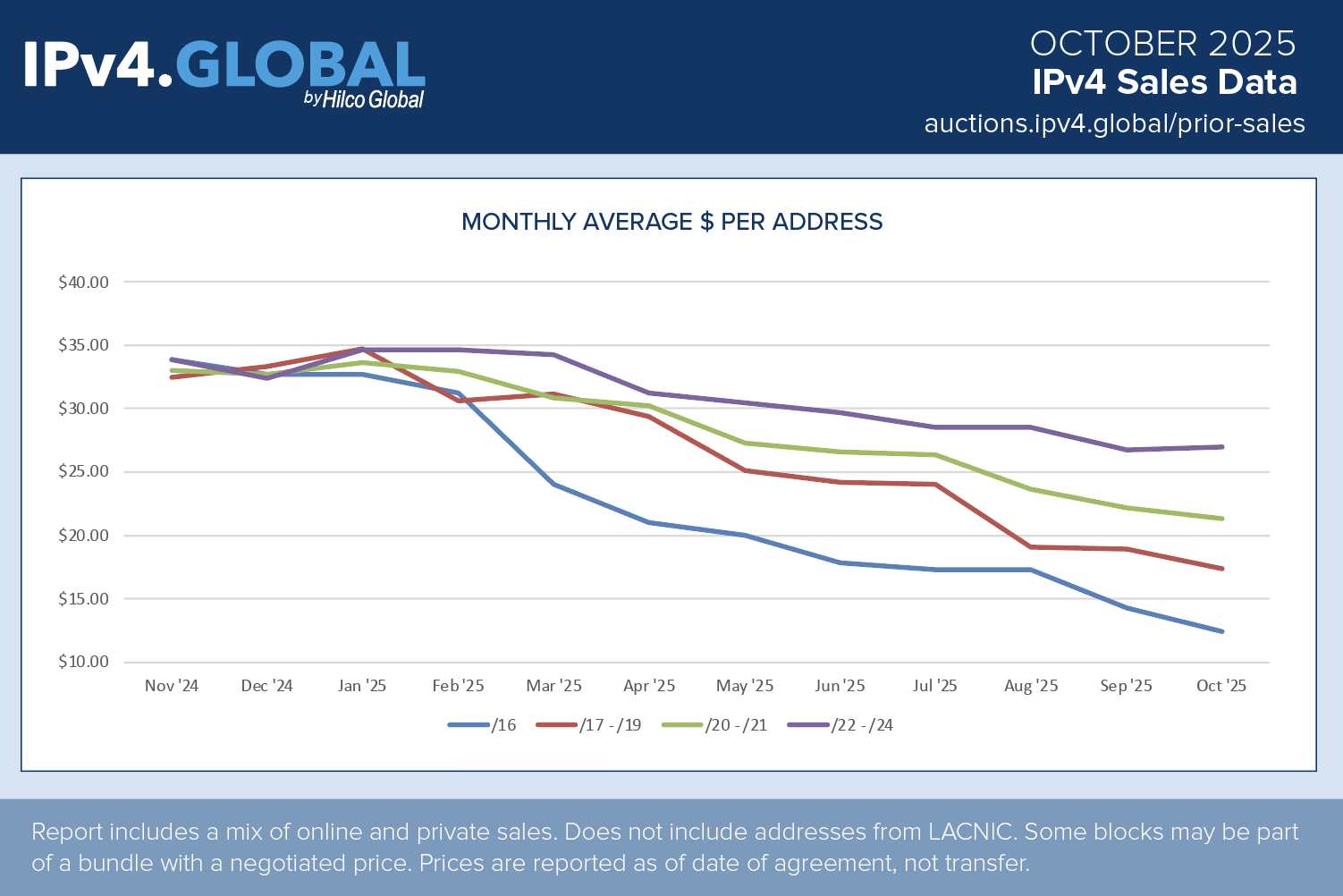

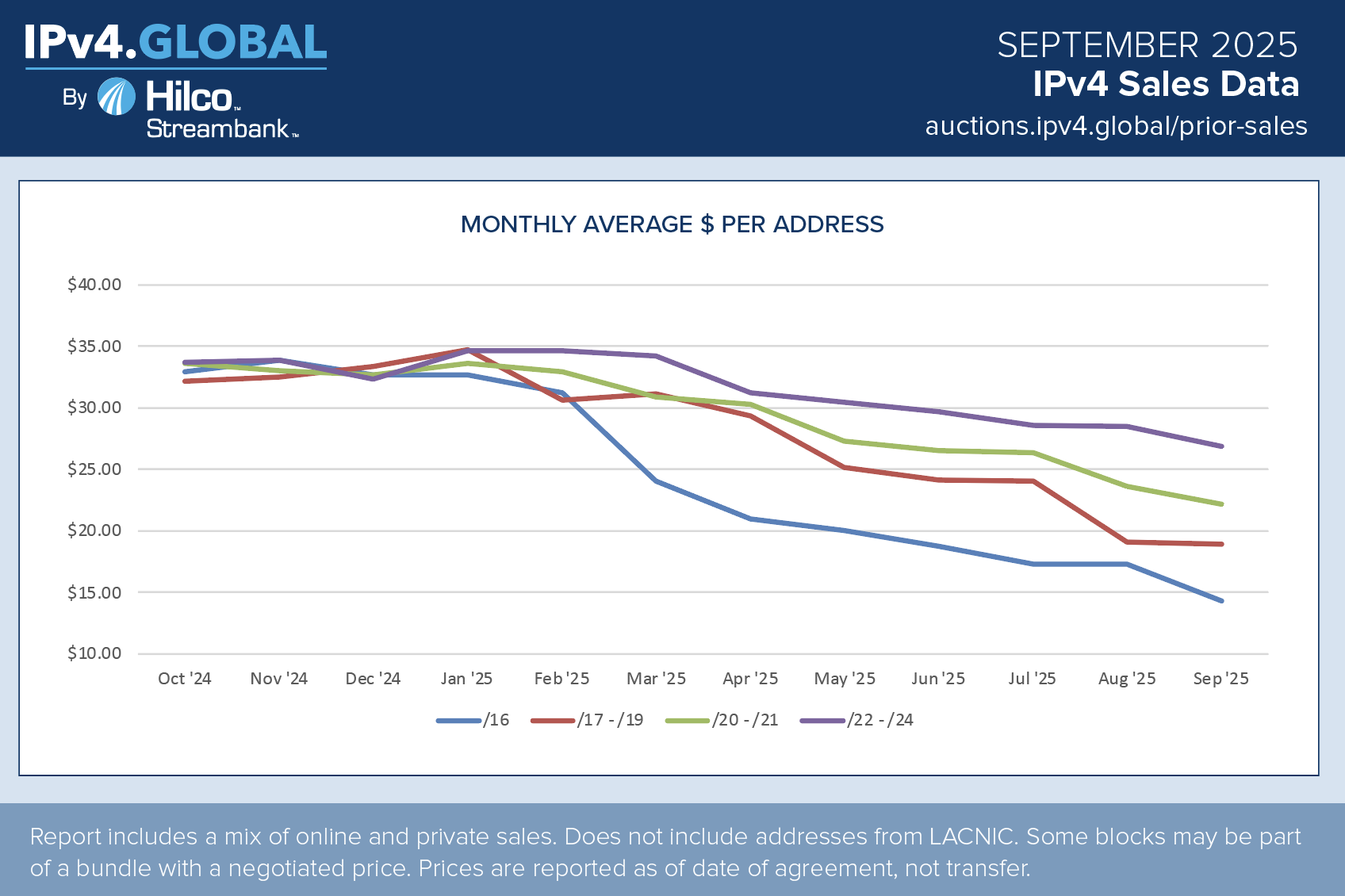

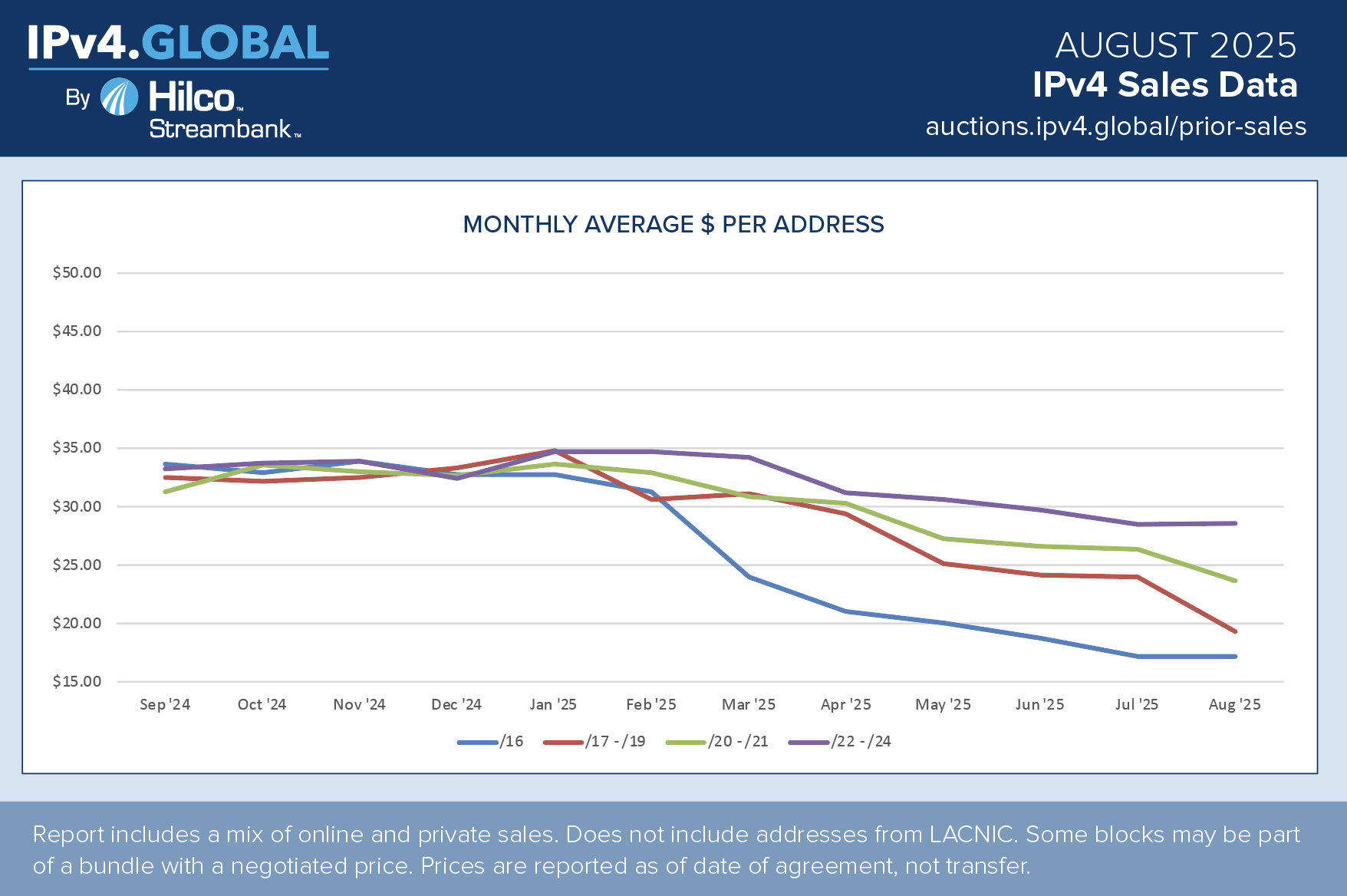

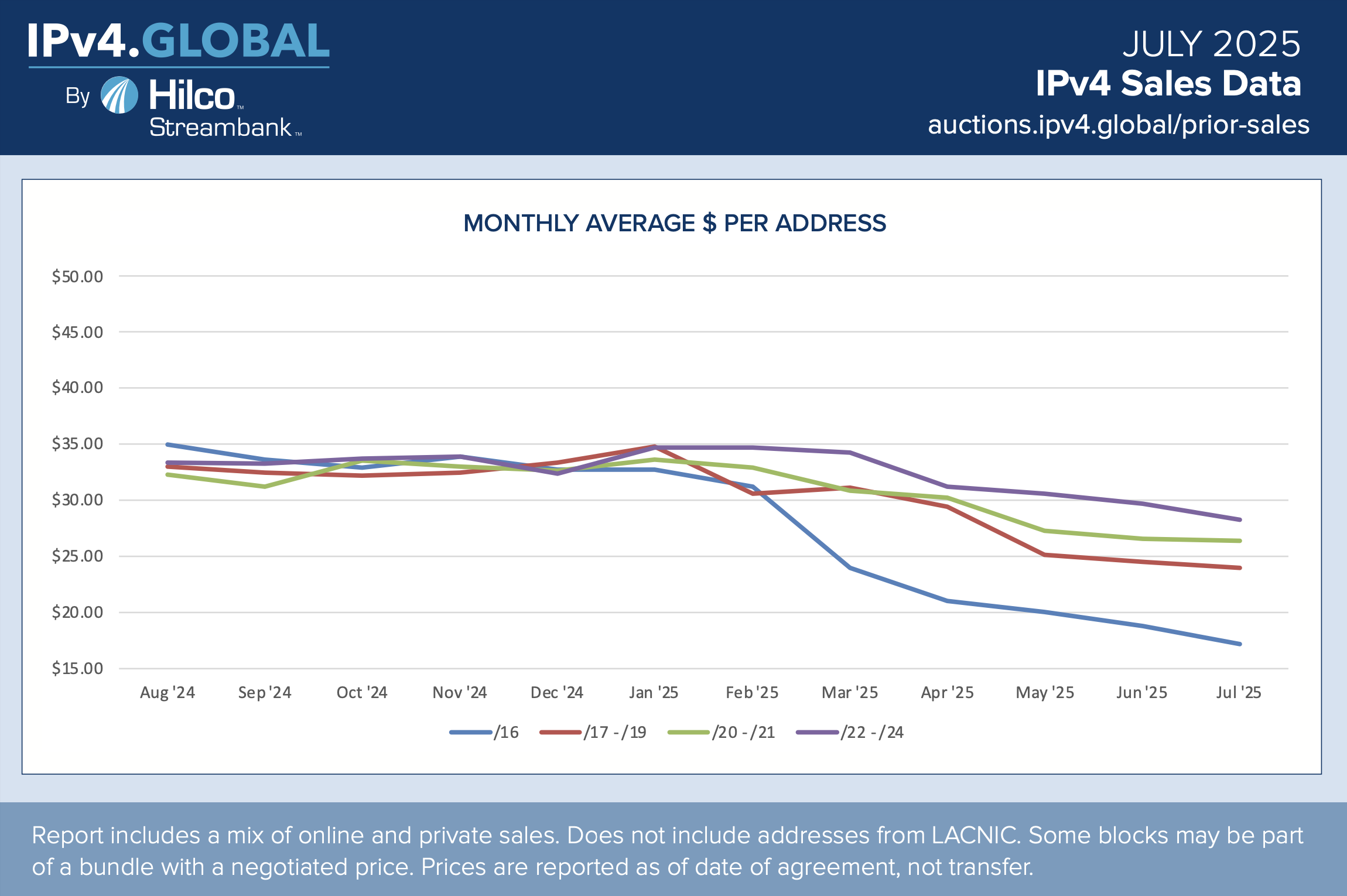

Are we seeing a true rebound in the IPv4 market? After a stable February where prices stopped their steady dip, we are now seeing a bit of an uptick. Volume and demand continue to be strong and diverse both by industry and region, with demand and volume for all block sizes. Based on trends we expect to see continued strength in this market.

Read more